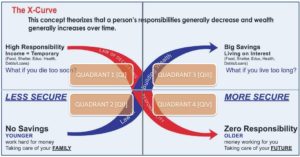

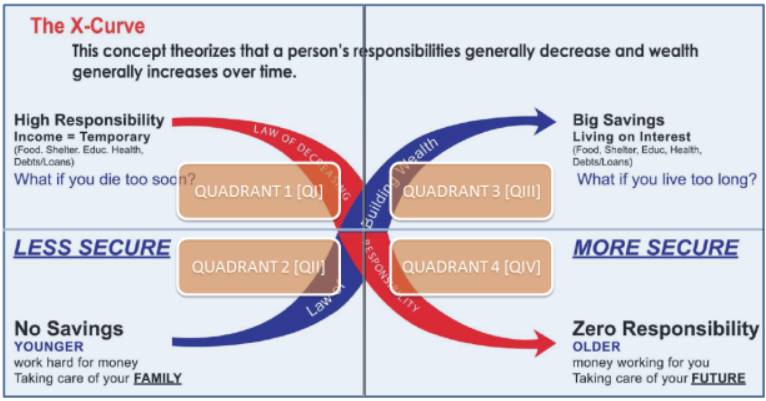

The X-curve is a graph showing two major lines in our lives: the wealth or savings line and our responsibility line. It is shown that ideally from younger to older years, our wealth and savings line should go up while our responsibility line simultaneously should go down.

The X-curve is divided into 4 quadrants. Quadrants I and II represents our younger years while III and IV represents our older years.

1. QI: shows that when we are young, we have very high responsibility. One of our major responsibilities is our income from our job or business. The challenge is that our income is usually temporary (nobody works forever) and our needs like food, shelter, clothing, education, etc. are permanent.

Thus, temporary income supporting permanent needs. It’s going to be very difficult to say:

“I’m now retired! I have no more income. I will also retire eating and taking a bath! What a comfortable life!” (sarcasm intended)

2. QII: in quadrant II, typically when we are young, we have little to no savings at all. That’s why we work hard for money to provide for our family and ourselves.

During our younger years, we are very less secure. The question we need to consider is:

what if we die too soon? Are we prepared? Is our family ready? Who will take care of them?

3. QIII:due to the challenges in our younger years, we need to solve this dilemma by moving to quadrant III. From younger to older years, we need to build wealth, we need to build our savings and investment lines. The goal is to accumulate enough savings that will support us during our retirement years. With enough savings and investments, we pair it with the right financial knowledge we can then move to quadrant IV.

4. QIV:in this quadrant having the right financial knowledge and enough savings and investment, we can enjoy a life of zero responsibilities. Why? Because this time, we now let money work for us. How?

During our older years, it should be expected that following and understanding the X-curve concept, we should be more secured at this time. The challenge would be:

what if we live too long and don’t have enough savings? Who will take care of us?What if we are not financially educated and we don’t invest our 3M savings? In 3 to 5 years time, it will be depleted and retire broke at age 65 and beyond. Ultimately, the key to wealth building is having the discipline to save and taking the time to learn financial education. Make sure to follow the x-curve concept in wealth building.